When you bring on subcontractors for your business, ensuring they have the right insurance coverage is crucial for protecting your bottom line and avoiding potential liabilities. One of the best ways to verify their coverage is by obtaining and carefully reviewing their Certificate of Insurance (COI).

Why You Need Your Subcontractors to Have Their Own Insurance

If your subcontractors don’t have their own workers’ compensation and general liability insurance, you might end up having to cover them under your policies, leading to increased premiums and potential complications during audits. Requiring your subcontractors to carry their own insurance is a fundamental step in protecting your business.

Getting Proof: The Certificate of Insurance (COI)

Don’t just take your subcontractor’s word for it – always request a COI as proof of their insurance coverage. A COI is a document that provides a snapshot of their insurance policies at a specific point in time.

Key Things to Look for on a Subcontractor’s COI

When you receive a COI from a subcontractor, carefully examine the following sections to ensure they have adequate and active coverage:

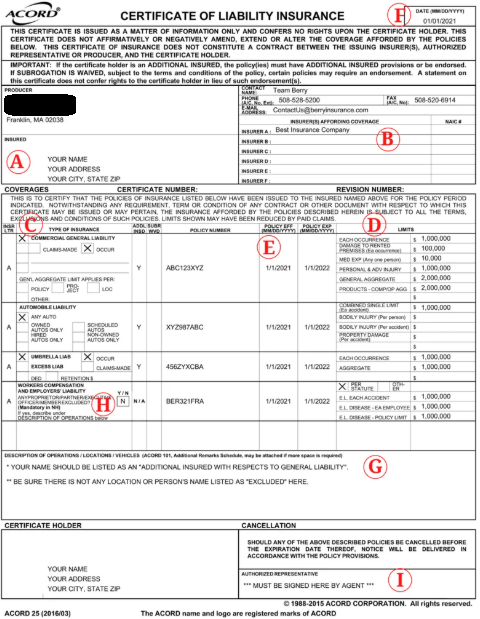

- A. Named Insured: This should clearly state the legal name of the subcontractor or their business.

- B. Insurance company: This section shows the insurance company your contractor has the business insurance policy through. Sometimes, there may be more than one insurance company listed. This just means they have different carriers for their different types of insurance. You’ll want to look at the insurance types section to make sure the correct policies correspond with the correct carriers.

- C. Insurance Types: Verify that the COI includes the types of insurance you require. For most subcontractors, this should include at a minimum:

- Workers’ Compensation: This covers their employees if they get injured on the job. Ensure the limits are adequate (we often recommend at least $500,000). Pay close attention to whether the owner/officer is included or excluded from coverage. If they are working on your project, they generally should be included.

- General Liability: This protects the subcontractor’s business against claims of bodily injury or property damage they cause to others. We often recommend at least $1 million in coverage.

- D. Limits: Check the policy limits for each type of insurance listed. Make sure they meet your minimum requirements.

- E. Policy Effective Date: Confirm that the policy is currently active and will remain active for the duration of your work with the subcontractor. If the expiration date is approaching, request an updated COI.

- F. COI Date Issued: Note the date the COI was issued. Remember that a COI only proves coverage was in place on that specific date.

- G. Special Conditions: This is a crucial section. Ideally, your company (“StreetSmart Insurance” if you want to use our agency name as an example, but generally your client’s business name) should be listed as an “additional insured” on the subcontractor’s General Liability policy. This provides you with direct coverage under their policy for claims arising from their work. Also, the specific project or job details should be mentioned here.

- H. Workers’ compensation: Under the workers’ compensation section, there will be a check box indicating whether the owner is included under the policy. Sole proprietors and officers of corporations can opt out of workers’ comp coverage, so the check box will show you whether they are included or not. There may also be language about it in the special conditions section if the owner is not included. If the sole proprietor or officer is one of your subcontractors you’ll need to make sure that the certificate spells out that they do have workers’ comp.

- I. Signature: Ensure the COI is signed by the subcontractor’s insurance agent, indicating it’s an official document.

Managing COIs for a Smooth Audit

If your business frequently hires subcontractors, establishing a system for collecting and organizing COIs is essential. This will streamline your workers’ compensation audits and help you avoid paying for uninsured subcontractors under your policy.

By taking the time to obtain and carefully review COIs from your subcontractors, you can significantly reduce your business risks and ensure a smoother, more protected operation.